Why Written Rules Do Not Protect Institutions When Controls Are Weak, Untested, or Ignored in Practice

Technical Staff

March 31, 2026

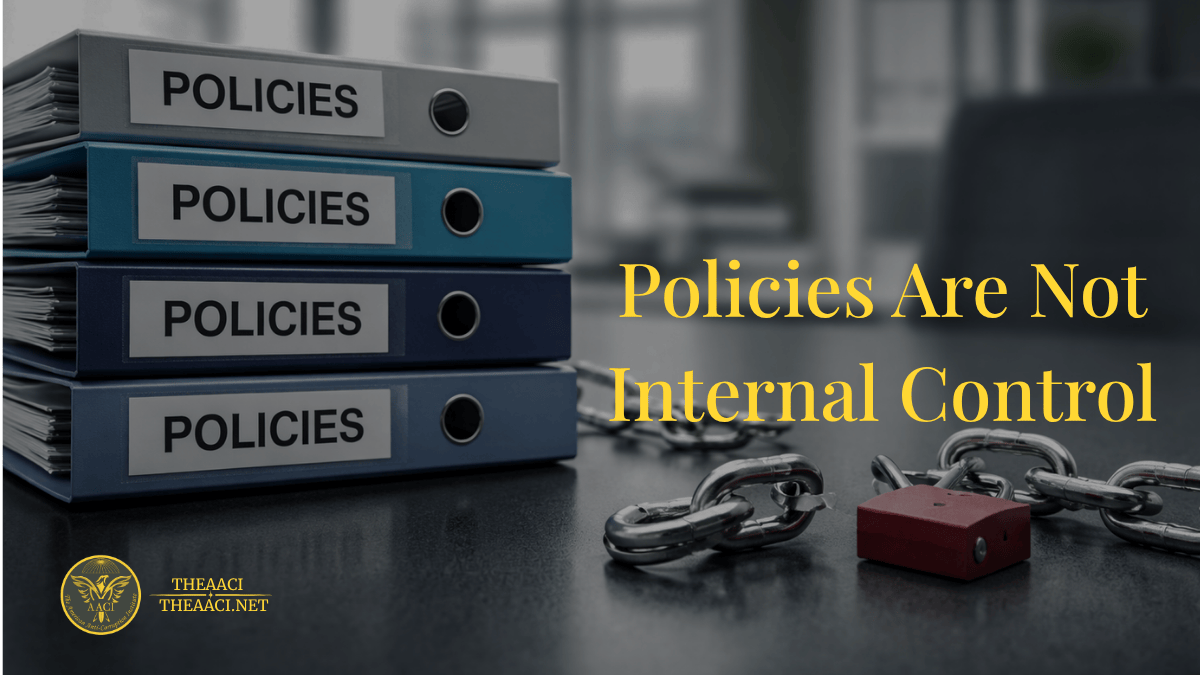

Many institutions take comfort in having policies. They point to manuals, approvals, formal procedures, and organizational charts as if these prove that risk is being controlled. They do not.

A policy is a statement of intention. Internal control is a system of action, verification, accountability, and discipline. Internal control is objective-oriented, aiming to achieve reporting, operations, and compliance objectives. Confusing one for the other is a serious governance failure.

This confusion persists because policies are visible. They can be approved, circulated, filed, and displayed. They create the appearance of order. Internal control is harder. It must function in practice, withstand pressure, restrict misconduct, expose irregularities, and continue working even when management preferences pull in the opposite direction. A policy may establish approval requirements. An effective internal control ensures that those approvals are informed, independent, documented, and resistant to management override.

That distinction matters because fraud and corruption do not usually enter through the absence of paperwork. They enter through weak execution, poor segregation of duties, unchecked discretion, passive review, and a culture that treats compliance as form rather than substance.

Boards and executive management should stop asking whether a policy exists and start asking whether the internal control actually works. Who tests it? Who can override it? Who monitors exceptions? Who challenges weak evidence? Who is held accountable when the control fails? Those are internal control questions. Simply approving a policy does not answer any of them.

The danger grows when institutions rely on written procedures to reassure themselves that the risk has already been addressed. That false comfort weakens skepticism, dulls oversight, and allows avoidable failures to mature quietly behind a facade of compliance.

Internal control is not a binder. It is not a committee chart. It is not a paragraph in a manual. It is a living discipline that must operate under real conditions and withstand real pressure.

Serious decision-makers should not be guessing on issues like these. Strengthening oversight of corruption risk, internal control, governance, and management judgment requires structured anti-corruption knowledge, not passive reliance on titles or experience alone. For professionals who want to sharpen their ability to distinguish between appearance and effectiveness, the CACM self-study pathway offers a disciplined body of knowledge designed for that purpose.